-1776244031.webp)

Introduction: Why Markets Shift After Geopolitical Stress

When geopolitical tensions rise, markets rarely move based on fundamentals. Instead, they most probably react to uncertainty, fear, and sudden disruptions, as per analyst analysis. Prices become more sensitive to headlines than to actual business performance, pushing some sectors well above or well below their perceived value.

However, once tensions begin to ease, even slightly, the market dynamic shifts. The focus moves away from immediate risk and back toward fundamentals such as demand, costs, and long-term growth. This transition phase is often where some sectors start to look particularly interesting, not because of speculation, but because of how they were previously affected.

Airlines: A Sector Built for Rapid Recovery

The airlines sector is a clear example of this shift. During periods of geopolitical stress, the sector faces a combination of rising fuel costs, weaker travel demand in affected areas, and operational disruptions. These pressures tend to weigh heavily on performance. However, when conditions stabilize, airlines often recover faster than expected. This is largely because the factors that pressured them begin to reverse at the same time.

· Oil prices tend to stabilize or decline, easing cost pressures

· Travel demand gradually returns as confidence improves

· Flight routes and operations become more predictable

This creates a situation where the downside was driven by uncertainty, while the upside is supported by normalization, which can occur relatively quickly, as per analyst analysis.

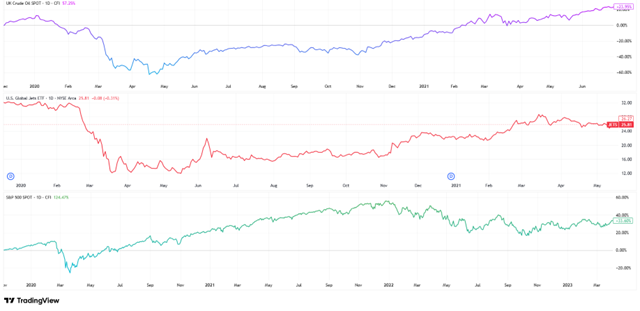

This dynamic is clearly reflected in the chart during the COVID-19 pandemic, where airline stocks (red) underperformed both oil (blue) and the S&P 500 (green), highlighting the sector’s sensitivity to rising costs and demand uncertainty (Figure 1). While the broader market recovered relatively quickly, airlines lagged before gradually improving as oil stabilized and travel demand returned. This reinforces the idea that airline performance is not driven by immediate market recovery, but by the easing of key pressures, allowing the sector to catch up once conditions begin to normalize.

Figure 1: UK Crude Oil (Blue line), U.S. Global Jets ETF (Red line), S&P500 (Green line), Daily time frame, 2020-2023, Source: Trading View

FMCG: Stable Demand, Recovering Margins

The FMCG (Fast-moving consumer goods) industry, on the other hand, behaves very differently. Unlike airlines, demand for everyday goods remains relatively stable even during periods of tension. Consumers continue to purchase essential items such as food, beverages, personal care products, etc. This helps companies maintain steady revenue. However, the real pressure often comes from rising input costs and supply chain disruptions, as per analyst analysis.

As tensions ease, the key shift for FMCG companies is not demand, but cost. With supply chains stabilizing and commodity prices normalizing, margins begin to recover. This positions the sector as a more gradual, but potentially steady, recovery story.

- Demand remains stable throughout both phases

- Cost pressures begin to ease after tensions subside

- Profitability improves as margins recover

Rather than a sharp rebound, FMCG tends to reflect a quieter improvement in financial performance.

This dynamic is clearly reflected in the chart during the recent inflationary period. While the S&P 500 (blue) experienced more pronounced fluctuations, the Consumer Staples Select Sector SPDR Fund (red) remained relatively stable, highlighting the sector’s resilience in terms of demand.

At the same time, the rise in input costs, as measured by the Invesco DB Agriculture Fund (green), coincided with periods when FMCG performance lagged (Figure 2). As these cost pressures began to stabilize and decline, the sector gradually improved, not through a sharp rebound but through a steady recovery.

This reinforces a key point: FMCG performance is less sensitive to demand shocks and more influenced by cost dynamics, with recovery driven by margin normalization rather than immediate market momentum.

Figure 2: US500 (Blue line), Consumer Staples SPDR (Red line), Invesco DB Agriculture Fund (Green line), Daily Time frame, 2021-2023, Source: Trading View

Defense: Long-Term Spending Outlasts Short-Term Tension

Defense stocks present another interesting dynamic. They typically benefit during geopolitical escalation due to increased government spending and heightened security concerns. However, a common misconception is that demand for defense declines once tensions ease. Spending often remains elevated as countries continue to prioritize long-term security and preparedness, as per analyst analysis.

This means the sector does not necessarily weaken; it transitions. The focus shifts from short-term reactions to longer-term planning, making it less driven by headlines and more influenced by policy and strategic priorities.

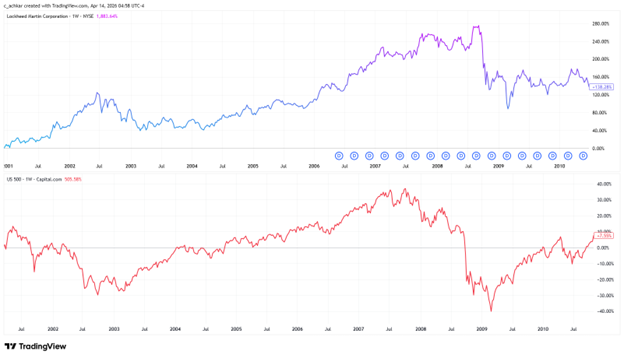

This dynamic is clearly reflected in the chart during the period following the September 11 attacks, which took place in 2001 in New York and Washington, D.C. In the aftermath, defense stocks such as Lockheed Martin (blue) outperformed the broader S&P 500 (red) over an extended period (Figure 3). Defense spending increased significantly and remained elevated, supporting the sector even as overall market conditions evolved. This divergence highlights a key characteristic of defense: performance is driven less by short-term market recovery and more by sustained government spending, allowing the sector to remain supported well beyond the initial shock.

Figure 3: Lockheed Martin Corp. (Blue line), US500 (Red line), Weekly Time frame, 2000-2010, Source: Trading View

Infrastructure: The Delayed Beneficiary of Stability

Infrastructure is often overlooked in this context, yet it plays a significant role once stability returns. During periods of uncertainty, governments and private entities tend to delay large-scale projects. Capital expenditure slows, and investment decisions are postponed. However, once conditions improve, infrastructure spending often resumes and can even accelerate.

- Governments use infrastructure to support economic growth

- Projects that were delayed are gradually reactivated

- Investment confidence improves alongside stability

This makes infrastructure less of an immediate reaction and more of a delayed beneficiary of easing tensions, particularly in regions with ongoing development plans.

The Broader Market Shift: From Sentiment to Fundamentals

Beyond individual sectors, the broader shift in market behavior is equally important. During geopolitical stress, markets tend to move collectively, driven by risk sentiment rather than selective analysis. Once tensions ease, this behavior changes. Investors begin to differentiate between sectors and companies, focusing on fundamentals such as earnings visibility, cost structures, and balance sheet strength.

This dynamic is reflected in the chart following the COVID-19 pandemic in 2020, where the S&P 500 (red) recovered relatively quickly, while infrastructure exposure, represented by the Global X U.S. Infrastructure Development ETF (blue), lagged before gradually improving (Figure 4). As government spending and stimulus measures supported the economy, infrastructure gained momentum over time, highlighting that the sector benefits from policy-driven recovery rather than an immediate market rebound.

Figure 4: Global X U.S. Infrastructure Development ETF (Blue line), US500 (Red line), 2018-2026, Weekly Time Frame, Source: Trading View

Conclusion

Oil remains a key driver across sectors. Higher prices increase cost pressures, while lower or stable prices support recovery and reduce uncertainty.

Ultimately, the opportunity lies not in the geopolitical event itself, but in what follows. As conditions stabilize, market distortions begin to correct, some quickly, others more gradually. The real shift occurs when markets move away from reacting to headlines and return to fundamentals.

-1785495783.webp)

-1724934015.webp)

-1785402917.webp)

-1785318371.webp)