Introduction:

Global markets are witnessing a significant set of economic events and indicators that are expected to cast a shadow over various assets and financial instruments.

These events begin with US economic indicators, continue with important meetings of three central banks, including the US Federal Reserve, and conclude with US economic indicators and a deadline for suspending US tariffs.

Although markets are preparing for both US labor market data and inflation data, the second-quarter GDP report may represent a positive turnaround for the US economy compared to the contraction seen in the first quarter.

Global markets will also focus on August 1, the date when the US tariff suspension against all countries that have not reached final trade agreements ends.

Main keywords:

The Federal Reserve holds its meeting amid ongoing tensions between the Trump administration and the US Federal Reserve Chairman.

The Bank of Canada and the Bank of Japan hold important meetings amidst divergent economic conditions.

Markets are monitoring extremely important economic data this week before and after the Federal Reserve meeting.

US GDP may rebound after a contracting first quarter.

Economy Spotlight. US Federal Reserve meeting in July 2025 with sensitive economic data

First, the US economy:

Last week saw several important events, particularly related to corporate earnings, particularly those of major companies represented by Alphabet (Google's parent company) and Tesla, the first of the Amazing Seven.

There were also significant developments in trade agreements, particularly with Japan, Europe, and other parties. In terms of economic data, many US companies achieved profits that exceeded expectations, apart from Tesla, which announced a decline in car sales revenue of approximately 16%.

Alphabet achieved profits that exceeded expectations, achieving $96.43 billion in the second quarter of this year, while pledging to increase spending on data centers. In terms of banks, JPMorgan reached a record high in share value at $286, with a market capitalization of approximately $814 billion, thanks to its strong second-quarter results.

Regarding economic data, it was a relatively quiet week, with home sales declining slightly and a decline in crude oil inventories. However, next week will be the most important week for the US economy.

US markets are facing a very crucial week:

US markets are preparing important economic data, led by the Federal Reserve meeting, with expectations that interest rates will not be cut.

This meeting will be preceded by highly significant data, specifically consumer confidence, job openings, and GDP, which includes the first reading for the second quarter of this year, indicating a significant improvement and an exit from the contraction the US economy experienced during the previous quarter.

Labor market data will then be followed by the Federal Reserve meeting, specifically regarding wages, unemployment, and the non-farm payrolls report.

All this data comes amid clear progress in trade agreements with important parties, most notably Japan, which has reached a complete reduction in tariffs, including on automobiles, by 15%, down from the previous 25%.

There were also agreements with important countries such as the Philippines, and US Treasury Secretary Scott Besant stated that there was a possibility of extending the suspension of tariffs with China beyond August 1.

US Commerce Secretary Howard Lutnick confirmed that efforts to reach trade agreements with the European Union were nearing a real breakthrough, despite US President Trump's assertion that the chances of reaching an agreement with the EU were now equal, especially considering the meeting between European Commission President Ursula von der Leyen and the US President.

As for trade talks with South Korea, they were postponed for reasons related to the US side, with strong hopes of reaching solutions soon in the coming days. Meanwhile, Trump announced the possibility of not reaching a trade agreement with Canada and Mexico.

Second. European Economy:

The trade agreement between the US and Japan represented optimism on the European side that satisfactory trade solutions would be reached soon, coinciding with tensions in relations between the European and Chinese sides.

This came after the European Commission announced that it had informed Chinese President Xi Jinping that the relationship between the two economies had reached a critical point and that efforts must be made to resolve many of the remaining problems.

Regarding Europe's largest economy, Germany, some 60 leading German companies pledged on Monday a major investment initiative called "Made for Germany," aiming to boost investor confidence in the country's economy and revive it.

Before heading into the European Central Bank's meeting to decide on interest rates, manufacturing data was released, one of the most promising economic indicators for the European economy.

The eurozone private sector grew at its fastest pace since August 2024, paving the way for the end of the three-year manufacturing recession. The composite Purchasing Managers' Index (PMI) also rose to 51, indicating that the services sector is moving away from the contractionary threshold of below 50.

Regarding interest rates, the European Central Bank kept interest rates at 2%, as expected, marking a pause after a year of monetary policy easing. Analysts interpreted this as a pause pending clarity on the future of trade relations between Europe and the United States. The ECB President indicated that the future of interest rates could only be determined considering economic data.

Third: The Japanese Economy:

While Japan's ruling coalition suffered a major defeat in the upper house elections, further complicating the position of the Bank of Japan, Japan was moving toward signing a trade agreement with the United States.

This agreement, which came at a very sensitive time, provided optimism and hope for saving the Japanese economy from the repercussions of tariffs, which would have further complicated the economic situation in Japan.

This agreement also represents a welcome respite for the Japanese economy, whose central bank is set to make its interest rate decision later this week, immediately after the US Federal Reserve meeting.

For their part, during the 30th EU-Japan Summit, leaders pledged to strengthen cooperation in the areas of security, competitiveness, and multilateralism.

For the second consecutive month, Japanese exports declined, with the auto sector suffering from US tariffs.

Pressure is expected to increase on the country, which is still struggling to control inflation while raising interest rates to save its currency.

With this positive news regarding enhanced cooperation between Japan and various major economies, optimism was high to save the Japanese economy from deflation or entering a recession.

Fourth: The Chinese Economy:

Economic disputes between China and Europe surfaced during a summit last week, prompting the European Commission to urge China to resolve these disputes quickly for the benefit of both sides.

This led to an agreement to ease tensions over rare earth mineral exports. The Chinese president also emphasized the need to combat the aggressive price competition by some Chinese companies, which is negatively impacting the Chinese economy at a critical time, especially given the ongoing housing downturn despite significant stimulus packages.

Regarding trade agreements with the US, especially with the August 1 deadline approaching, Treasury Secretary Scott Besant announced plans to address China's economic imbalances, highlighting progress made in reducing tariffs and shifting focus to broader issues with China.

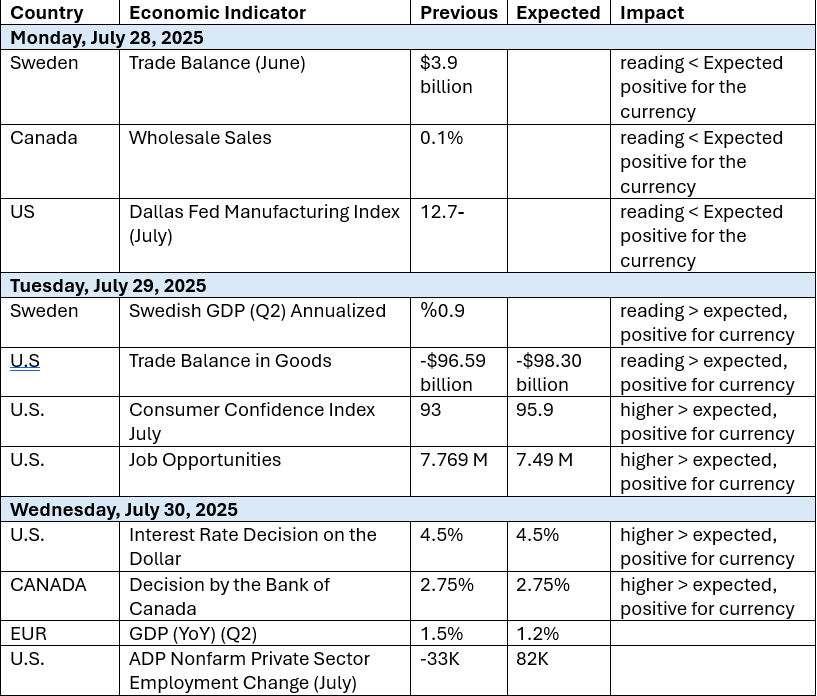

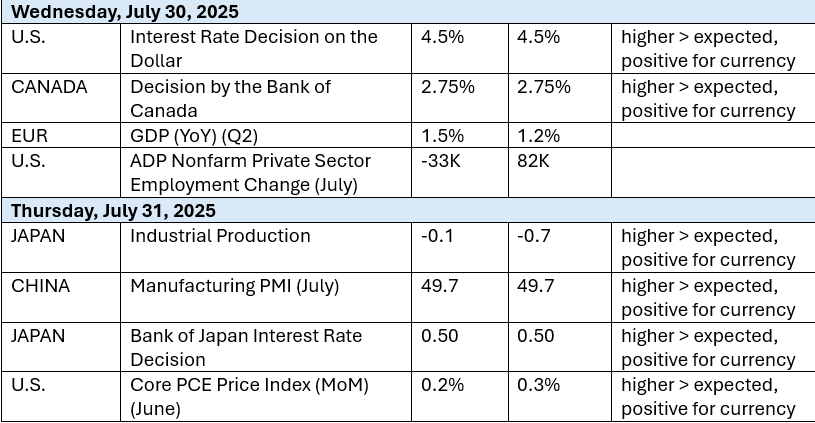

Economic Calendar After the Federal Reserve Meeting July 2025: What to Expect in the Markets

Global markets will be awaiting the following economic data:

-1724934015.webp)