-1777548306.webp)

Key Takeaways

- AI has evolved from an experiment into a large-scale capital cycle reshaping financial markets.

- The AI ecosystem can be understood in three distinct layers: infrastructure, utilization, and services.

- Each layer captures value differently, and not all AI-related companies benefit equally.

- High capital expenditure does not always translate into sustainable profitability.

- AI is redistributing value across markets, creating winners and laggards across sectors.

Why AI Has Become a Capital Cycle

Artificial Intelligence is no longer just a technological trend. It is becoming a capital cycle that is reshaping financial markets.

Over the past few years, companies have moved beyond experimentation. What we are seeing today is a shift toward large-scale commitment, with hundreds of billions of dollars being allocated toward building, integrating, and scaling AI capabilities.

This is already influencing how markets behave. Prices no longer react only to earnings or macroeconomic data. Increasingly, they are reacting to AI-related developments, investment levels, adoption progress, and long-term positioning, as per analyst analysis.

This shift is also reflected in how industry leaders think about this space:

"I'd rather risk misspending a couple of hundred billion dollars than miss the opportunity."

Mark Zuckerberg

This highlights the scale of the transition. AI is no longer being approached as an experiment but as a long-term investment cycle in which positioning matters.

Understanding the AI Ecosystem: A Three-Layer Structure

To better understand how AI is influencing financial markets, it helps to break the ecosystem into three core layers.

Rather than viewing AI as a single trend, it is more accurate to see it as a connected value chain. Each layer plays a different role in the creation, capture, and eventual reflection of value in market performance.

At a time when AI-related companies are attracting significant capital flows, this distinction becomes important. Not all parts of the ecosystem benefit in the same way, even if they are all linked to the same theme.

The three layers can be simplified as follows:

- Infrastructure: the foundation that powers AI

- Utilization: how companies apply AI in their operations

- Services: where AI becomes a product and generates revenue

At a high level, the relationship between these layers is straightforward: Infrastructure enables AI, utilization drives productivity, and services determine how productivity translates into financial results.

This structure is also reflected in how market participants are approaching this space. As Jensen Huang, Nvidia's co-founder, president, and chief executive officer, has repeatedly emphasized, demand for AI infrastructure is being driven by a global shift toward accelerated computing, highlighting that the foundation layer is attracting a significant share of capital investment.

However, from a market perspective, the key takeaway is this: each layer captures value differently.

Some companies benefit directly from capital spending (infrastructure), others from efficiency gains (utilization), while a smaller group converts AI into scalable revenue streams (services).

This is why, even within the same AI theme, performance can vary significantly across stocks.

Understanding where a company sits within this structure is not just a technical detail. It is often the difference between capital being deployed and value being created.

Layer 1: Infrastructure (The Foundation of AI)

At the base of the AI ecosystem sits infrastructure, the physical and technological backbone that makes AI possible.

This layer includes:

- Semiconductor (GPUs, CPUs): the processors responsible for handling AI computations and data processing

- Data centers: large-scale facilities where AI systems are trained and deployed

- Cloud computing systems: platforms that provide access to AI capabilities without requiring in-house infrastructure

- Energy and cooling solutions: the systems needed to power and maintain these operations efficiently

Companies such as NVIDIA have become central to this layer, supplying the chips that power advanced AI models. At the same time, TSMC manufactures these chips, while ASML provides the critical machinery required to produce them.

The importance of this layer is straightforward: without infrastructure, AI cannot scale.

Training advanced AI models requires significant computing power. In some cases, the cost of training a single model can reach hundreds of millions of dollars. This has triggered a global push to expand data centers and increase computing capacity.

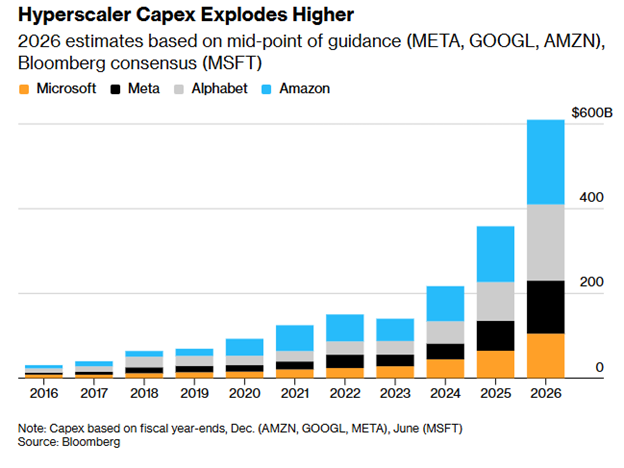

This shift is already visible at the industry level, with major technology companies significantly increasing capital expenditure to support AI infrastructure (Figure 1).

Figure 1: Hyperscaler capital expenditure growth reflects the scale of AI infrastructure investment, Source: Bloomberg

This trend is also being reflected at the industry level. As Jensen Huang noted:

''The next industrial revolution has begun ... companies and countries are investing in AI infrastructure.''

Jensen Huang

From a market perspective, this layer shares similarities with the early stages of a gold rush:

- High demand

- Limited supply

- Strong pricing power

This combination has supported strong revenue expectations for infrastructure-related companies, with capital flowing heavily into this segment.

However, one key consideration remains:

High capital expenditure does not always translate into sustainable profitability.

While infrastructure providers may benefit early in the cycle, the long-term outcome depends on whether this investment leads to consistent demand and monetization across the broader AI ecosystem.

Layer 2: Utilization (Turning AI Into Productivity)

The second layer is where the real transformation begins.

This is no longer about building AI; it is about using it effectively. From a market perspective, this is where the narrative starts to shift away from pure investment and toward operational performance.

Companies in this layer integrate AI into their day-to-day operations to:

- Improve efficiency

- Reduce costs

- Enhancing decision-making

- Create new products and services

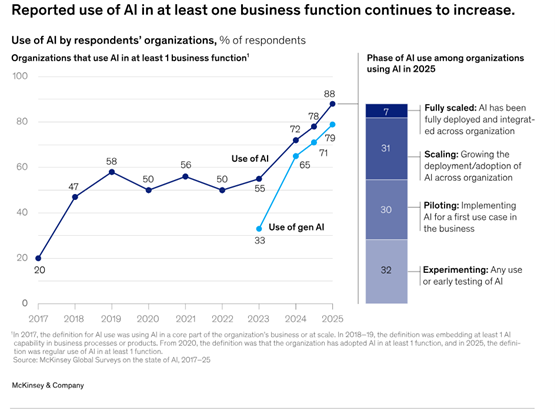

This shift is already visible at the global level, with a growing number of companies moving from experimenting with AI to actively deploying it across their operations (Figure 2).

Figure 2: Global AI adoption continues to rise as companies move from experimentation to deployment, Source: Mckinsey & Company

This transition is already visible. The growth in cloud infrastructure reflects how AI is moving beyond development and into real-world applications. As adoption increases, companies are relying more on cloud platforms to deploy, scale, and integrate AI across their operations.

This can be seen across major players:

- Microsoft is embedding AI into productivity tools and enterprise software

- Alphabet enhancing search, advertising, and data analytics

- Amazon is optimizing logistics, cloud services, and automation

From a market perspective, this layer is critical because it determines whether AI spending translates into real economic value.

A simple way to understand this layer is through a familiar analogy:

AI infrastructure is like electricity. Having electricity alone does not create value; what matters is how it is used. The same applies to AI.

Some companies will use it to:

- Improve margins

- Increase efficiency

- Scale operations faster

Others may invest heavily but struggle to generate meaningful returns. This is why markets are gradually shifting their focus. It is no longer just about how much companies spend on AI, but about how effectively they use it. In other words, AI utilization efficiency is becoming more important than AI investment itself.

Layer 3: Services (Where AI Meets the End User)

The final layer is where AI becomes visible in everyday applications.

This is where its impact starts to show directly in revenue and financial performance. While infrastructure and utilization focus on building and applying AI, this layer is about turning AI into a product.

It includes:

- Software platforms

- Customer-facing tools

- Industry-specific AI solutions

This is where companies begin to monetize AI. For example, Salesforce uses AI to enhance customer engagement and forecasting, while Adobe integrates AI into creative workflows to improve productivity and user experience.

In financial markets, the impact is already visible across:

- Algorithmic trading

- Risk management systems

- Market analysis tools

At this stage, AI moves from being a capability to becoming a revenue driver.

As Satya Nadella, who has served as Microsoft's chairman since 2021 and as chief executive officer since 2014, highlighted:

“Every application will be rebuilt with AI at its core.”

Satya Nadella

From a market perspective, this is where outcomes become measurable:

- Revenue growth starts to reflect AI adoption

- Margins can improve through automation and scalability

- Competitive advantages become clearer across companies

However, this is also where disruption becomes more visible. Some companies can leverage AI to enhance their services and scale efficiently. Others face increasing pressure as AI-driven solutions begin to reshape traditional business models. In this layer, AI not only creates value; it also redistributes it. And this is where the difference between winners and laggards becomes most evident in market performance.

Conclusion

Looking at previous technological shifts provides useful context. AI is not the first time markets have gone through a transformation of this scale. During the dot-com era, companies invested heavily in internet infrastructure. Many failed, while a few, such as Amazon, emerged as long-term winners.

A similar pattern was seen with cloud computing. Early investment cycles were capital-intensive, returns were not immediate, but over time, clear leaders began to capture most of the value.

Not every company benefits equally during a technological shift. From a market perspective, AI is now entering a similar phase.

On one side, the opportunities are clear:

- Infrastructure demand remains strong as AI models require increasing computing power

- AI utilization can improve productivity, reduce costs, and support margin expansion

- New industries and business models are starting to emerge across sectors

However, the risks are equally important to consider:

- The gap between spending and returns remains uncertain

- Market exposure is becoming increasingly concentrated in a small number of companies

- Infrastructure constraints, particularly energy demand, could limit growth

- Disruptio risk is rising as AI reshapes existing business models

Bringing this together, AI is not just creating value; it is redistributing it across the market.

Some companies are positioned to capture long-term gains, while others may face increasing pressure as the cycle develops.

From a broader perspective, this reinforces a key point:

AI should not be viewed as a single theme, but as a multi-layered investment cycle where outcomes will vary significantly across companies and sectors.

-1783951441.webp)

-1724934015.webp)

-1782382125.webp)

-1782126200.webp)