-1776062280.webp)

The Week That Could Reshape Rate Expectations

Every so often, a single week of economic data has the power to shift the narrative for entire asset classes, this is one of those weeks.

From U.S to Europe, from Japan and China, major economies are releasing data that will tell us whether inflation is truly cooling or quietly picking back up.

At the center of it all sits one indicator that doesn't get enough credit: the Producer Price Index (PPI), and this week's reading could be the most consequential in over two years.

What Is the Producer Price Index (PPI)?

Think of the PPI as inflation's early warning system for inflation. While most people track the Consumer Price Index (CPI), the price you pay at the register, the PPI measures what producers pay upstream: raw materials, energy inputs, manufacturing costs.

Why Should traders and investors Care about PPI?

Because producer costs today become consumer prices in future, when factories and suppliers start absorbing higher costs, they eventually pass them on.

That makes the PPI one of the clearest leading indicators of inflation that central banks like the Federal Reserve watch closely.

In short: The Producer Price Index (PPI) tracks inflation before it reaches consumers' pockets. When the Consumer Price Index (CPI) rises, producers have anticipated this month in advance.

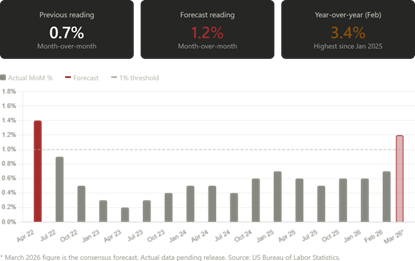

If the forecast of 1.2% MoM holds, this would mark the highest PPI reading since April 2022, and the first time the index has broken above the 1% barrier since that date.

On a year-over-year basis, February already came in at 3.4%, the highest since January 2025.

Together, these figures suggest that cost pressures aren't vanishing, they may be quietly re-accelerating.

Reasons for the PPI Is the Market's Most Important Number Right Now!

1. The energy shock transmission test.

The PPI is the first place those shocks show up in official data, a high reading confirms the energy shock is feeding into the broader economy.

2. The Fed's next move:

The latest CPI came in at 3.3%, just under the 3.4% consensus, and while that gave the Federal Reserve some breathing room to hold rates steady, a hot PPI print could complicate that calculus.

Performance of Major Economies

1. The United States: PPI Index, calm and watchful!

Markets across the board will be closely monitoring the March Producer Price Index reading. This figure takes on particular significance in the context of the oil price shock, as the PPI is widely regarded as one of the first indicators to reveal how energy price disruptions transmit through the broader economy.

Analysts argue that the energy price shock has so far failed to produce a meaningful spillover into other goods and services markets within the US economy. This dynamic raises the stakes for the upcoming April inflation print — and may give the Federal Reserve grounds to look past the latest CPI reading, which came in elevated at 3.3%, just a touch below the 3.4% consensus forecast. Taken together, these factors tilt the balance toward holding interest rates unchanged.

Analysts also note that forward-looking surveys are set to command considerable attention from markets, given their ability to capture investor sentiment around sector-level exposure to the energy shock. The two gauges to watch are the Empire State Manufacturing Survey and the Philadelphia Federal Reserve Index. Additional data releases of note include industrial production figures and weekly initial jobless claims.

2. Europe: Inflation Data Put to the Test

Market attention will converge on inflation readings from several major economies, with Eurozone CPI on Thursday drawing the sharpest focus. The release carries heightened significance given the European Central Bank's apparent openness to raising interest rates at its next meeting later this month.

Separately, the United Kingdom will publish its February GDP figures, with expectations pointing to a modest improvement following the economy's flat performance in January.

3. Asia: Decoding the Path of Japanese Rate Policy

Investors will be parsing every word of the Bank of Japan Governor's speech, searching for any signal regarding a potential interest rate hike. Those hopes have already dimmed somewhat for the April meeting, partly because of the two-week ceasefire agreement — a development expected to ease near-term inflationary pressures.

In China, a broad set of economic releases will be under the microscope. March trade data will be published alongside first-quarter GDP growth figures, with forecasts pointing to year-over-year expansion of 4.9% — an improvement on the 4.5% recorded in the final quarter of last year, though still well below the 5.4% posted in the comparable period a year prior.

Rounding out the data calendar, retail sales, fixed-asset investment, and industrial production figures will offer a read on the consumption and investment dynamics that are central to rekindling China's domestic economic momentum.

-1779607070.webp)